Retirement Income Planning · Business Owner Planning · Family Wealth Transfer & Legacy Planning

Don't ask the market for permission to Retire

We build tax-efficient retirement income strategies designed to be predictable — regardless of market conditions.

Serving pre-retirees and retirees nationwide from Jackson, MS and Chapel Hill, NC.

What We Do

Tax-Efficient Retirement Income Planning — Built Around Your Life

Branning Wealth Management is a fee-only, fiduciary financial planning firm specializing in tax-efficient retirement income planning. We help pre-retirees and retirees build income strategies designed to be predictable — regardless of market conditions — so you can stop losing sleep over what the market does tomorrow.

Our Safety-First approach begins with your income, not your returns. We build a foundation that funds your essential expenses first, then invest your remaining assets for long-term growth. The result is a retirement plan that doesn’t need the market’s permission to work.

Who We Work With

Pre-Retirees (50s–60s)

You’ve spent decades doing the right things — saving, investing, building. Now the question has changed. It’s no longer “how do I grow this?” It’s “how do I turn this into income I can actually live on?” That’s a fundamentally different problem. And it requires a fundamentally different kind of plan.

The ten years before retirement are the most consequential financial planning window most people will ever have. The decisions made in this period — when to retire, how to structure your income, how to sequence your withdrawals, when to convert to Roth, when to claim Social Security — compound in ways that affect your financial life for decades. We help pre-retirees build a tax-efficient retirement income strategy designed to be predictable from day one, so you can retire on your timeline — not the market’s.

already retired

Retirement isn’t the finish line. It’s the beginning of a 20–30 year financial planning challenge that most people aren’t told about until they’re already in it. Once you’re drawing income from your portfolio, the rules change entirely. A market downturn that was noise during your accumulation years becomes a real threat to your income if your plan isn’t structured to absorb it.

We work with retirees who want to know their income is genuinely protected — not just probable. That means coordinating Social Security, RMDs, Roth conversions, and withdrawal sequencing to minimize taxes year by year, structuring your income so a market decline doesn’t force you to sell at the wrong time, and adjusting the plan as tax laws, Medicare costs, and life circumstances change. Retirement income planning doesn’t end when you retire. For our clients, it’s when the real work begins.

business owners & Legacy planning

Not every client is counting down to retirement. Some are building — and planning to pass it on. If your goal is preserving and transferring wealth to the next generation, the same planning discipline that protects retirement income applies to what you're building right now.

For some, that means transferring wealth to children or heirs — intentionally, tax-efficiently, and on your terms. For others, it means the financial decisions made in the years before a sale: how you structure the transaction, how you plan for the tax consequences, how you begin transitioning from business income to personal income — decisions that are often more consequential than the sale itself.

We work with business owners at every stage: building tax-efficient wealth strategies before a transition, coordinating the financial planning around a sale or succession, and building sustainable income on the other side. Don't ask the market for permission to retire. Build the plan before you need it.

Professional athletes & college athletes

A professional athletic career creates a financial window that most people never experience — and that closes faster than anyone expects. For current and former professional athletes, we build tax-efficient income strategies designed to last for decades beyond the final paycheck.

For college athletes navigating NIL income for the first time, we help establish the financial habits, tax strategies, and planning foundation that will determine what options are available long after the playing days end. Kelly Jennings, CFP®, CDAA™ — a former University of Miami Hurricane and NFL wide receiver — leads this work at Branning Wealth Management. He's lived the transition at both the college and professional level. He knows what it takes to build something lasting from a career with a finite window.

Women & Primary Decision-Makers

Women face a retirement income challenge that doesn’t get enough attention: on average, they live longer, accumulate less over a lifetime due to career patterns and caregiving gaps, and are more likely to face widowhood, divorce, or a sudden shift in financial responsibility. These aren’t just statistics. They are planning variables that should shape a retirement income strategy in concrete, specific ways.

Longer life expectancy means your income needs to last longer — and your Social Security timing, Roth conversion strategy, and withdrawal sequencing all need to account for a 30-year retirement, not a 20-year one. Career gaps mean tax-efficient planning matters even more, because every dollar saved from unnecessary taxes is a dollar that stays in the plan. And for women who are the primary financial decision-maker in their household — whether by choice or circumstance — having a strategy that accounts for what’s most likely for you, not just the statistical average, is what separates a good plan from a plan that actually works. Kristi Tidwell, CFP®, CDFA®, TPCP® leads this work at Branning Wealth Management, bringing both technical expertise and personal understanding to every client relationship.

Retirement Planning Built on Research — Not Rules of Thumb

Our approach is grounded in Modern Retirement Theory (MRT), a proprietary retirement planning framework co-developed by Jason Branning, CFP®, RICP®, and published in The Journal of Financial Planning. MRT is now part of the Retirement Income Certified Professional® (RICP®) curriculum — meaning the methodology we use with every client is recognized as a national standard in retirement income planning.

The foundation of MRT is simple: retirement is an absolute goal, not a relative one. You want to retire and stay retired. That means your income plan has to be built around what you can count on — not what the market might do. We organize every client’s financial life into four strategic areas: your Base Fund (essential income), Contingency Fund (life’s surprises), Discretionary Fund (lifestyle goals), and Legacy Fund (what you leave behind). This structure gives your retirement plan clarity, purpose, and staying power.

unbiased

We act solely in your best interest—no commissions, no sales pressure, just clear guidance built around your goals.

Practical

Our Branning MATCH process uses data-driven, research-backed methods to align your resources with your life plans.

experienced

With decades of combined expertise, our advisors deliver professional, approachable service that makes planning feel simple and personal.

Our Philosophy

How We Build Your Retirement Income Plan: The Branning MATCH Process

Every client starts with the Branning MATCH process — a structured, data-driven approach that connects your income needs with your investments and resources. We don’t start with your portfolio. We start with your life: what you need, when you’ll need it, and how to fund it as tax-efficiently as possible.

The result is a retirement income plan built around what you can count on — not what the market might provide.

Get Started

Is your retirement income built to last?

If you’re within ten to fifteen years of retirement — or already there — and you want a tax-efficient retirement income plan built around what you can count on, we’d welcome a conversation. Serving clients nationwide from Jackson, MS and Chapel Hill, NC

Contact Us

We will get back to you as soon as possible.

Please try again later.

Not Ready Yet? Sign Up for Our Communications

Contact Us

We will get back to you as soon as possible.

Please try again later.

Blog

Featured Articles

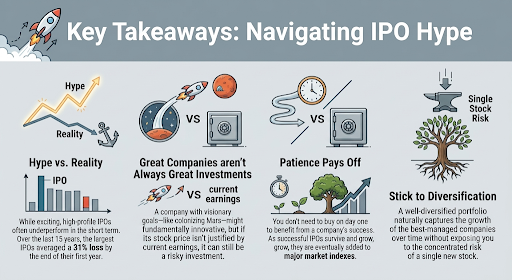

“To Infinity and Beyond”: The IPO of SpaceX

Over 50 and Eyeing Retirement