How Trump Accounts Work: A Financial Planner’s Guide for Parents

You’ve probably heard about “Trump Accounts” by now. On the surface, the idea is fairly simple: the government puts money in an account for your child, it gets invested, and then it grows over time.

But as with most things in the U.S. tax code, the reality is a bit more nuanced. While the prospect of "free money" is exciting, the real question for parents isn't just "how do I get it?" but how does this account fit into the rest of my financial plan?

So, what exactly are these accounts, how do they work, and most importantly, how should they fit into your overall strategy? Let’s take a look.

________________________________________________________________________________________________________________________

But first, let me introduce myself - I’m Johnson!

I help young professionals, families, and those near and in retirement build plan-first financial strategies designed to answer one important question: “Am I going to be okay?”

If you’re looking to strengthen your family’s financial plan, you may also enjoy:

- 10 Financial Moves To Make When You Have A Baby

- 7 Financial Essentials to Know Before Buying a Home

- What The Stock Market Is And Isn’t

- Emergency Funds: How Much Is Really Enough?

Back to the article!

________________________________________________________________________________________________________________________

What Is a Trump Account?

Trump Accounts (also known as “530A” accounts) are tax-advantaged, custodial investment accounts built to help children accumulate long-term wealth.

Think of them as a hybrid between a UTMA and an IRA . As a reminder:

- A UTMA is a custodial investment account that allows an adult to save and invest on behalf of a child, with the assets transferring to the child at adulthood.

- An IRA is a tax-advantaged retirement account designed to help individuals save and invest for retirement while receiving potential tax benefits.

The idea behind Trump accounts is to give kids a financial head start that allows money to compound over time alongside the broader U.S. economy. The initial legislation passed in July 2025 under the “One Big Beautiful Bill”, but these accounts aren’t actually expected to be available for enrollment and funding until July 2026 .

"Free Money"?

This is the part you hear the most about. Here is the gist of the "free" money:

- The $1,000 Seed Contribution : Children born between 01/01/2025 and 12/31/2028 are eligible for a one-time $1,000 deposit from the U.S. Treasury.

- No Match Required: Unlike many workplace 401(k) plans, you don’t have to contribute a dime to get the $1,000. It’s a government-funded starting point, not a match.

- Bonus "Starters": Some children may qualify for an extra charitable contribution ($250-$1,000) based on household income and ZIP code. Additionally, some specific states and companies offer their own incentives. This is ever-changing.

How to Set One Up

If you have (or are expecting) a child, here are the pretty straightforward requirements to be eligible to open a Trump account:

- Your child must be a U.S. citizen.

- They must have a Social Security Number.

- They must be under age 18 at the time of enrollment.

- Note: while children <18 may be eligible to open an account, only children born within the specified date range qualify for the government-funded $1,000 seed contribution.

To actually open the account , you can opt-in when filing your tax return (via a new IRS form) or enroll through the official online portal here → Trump Accounts.

How Do Personal Contributions Work?

Beyond the initial $1,000 from the government, anyone can contribute up to $5,000 per year, per child. This could be a parent, grandparent , friend… anyone. Sidenote: the government’s $1,000 contribution does not count toward this annual limit.

How Is The Money Invested?

Trump Accounts have clear rules on how funds can be invested before age 18:

- Low-Cost Only: Funds must be invested in low-cost, diversified U.S. stock funds. The expense ratios on these funds cannot exceed 0.10% , which is a good thing!

- At age 18: The account converts to a Traditional IRA , and these investment restrictions are lifted, giving you full flexibility in how the assets are invested going forward.

Tax Treatment

One important point that is often misunderstood: Trump Accounts are tax-deferred , but not tax-free like a Roth IRA.

- The Good: Personal contributions are made with after-tax dollars, and the account grows tax-deferred.

- The “Catch”: While you can withdraw your original contributions tax-free, any earnings withdrawn are taxed as ordinary income , similar to W-2 income.

- Restrictions: You cannot withdraw funds before age 18. After 18, a 10% penalty applies unless the funds are used for "Qualified Purposes" like education, a first-time home purchase, starting a business, etc.

While these accounts are not as tax-efficient as the mighty HSA, they still provide a powerful tax advantage through years of tax-deferred growth.

________________________________________________________________________________________________________________________

The Takeaway

These accounts are not a silver bullet, but they can be a valuable tool.

How You SHOULD Use Trump Accounts:

- Take advantage of the "Seed": If you’re eligible for the $1,000, take it . It’s essentially a "free lunch" from the Treasury.

- Think Decades, Not Years: Treat this as a long-term investment account, not a short-term savings account.

- Coordinate: Use it alongside 529 accounts (for education) and Roth IRAs (if the child has earned income).

How You SHOULDN’T Use Trump Accounts:

- Don't "Solo" It: Don’t treat this as your only savings strategy for your child.

- Don't Ignore Taxes: Remember that there is a tax bill waiting when funds are withdrawn. Plan accordingly.

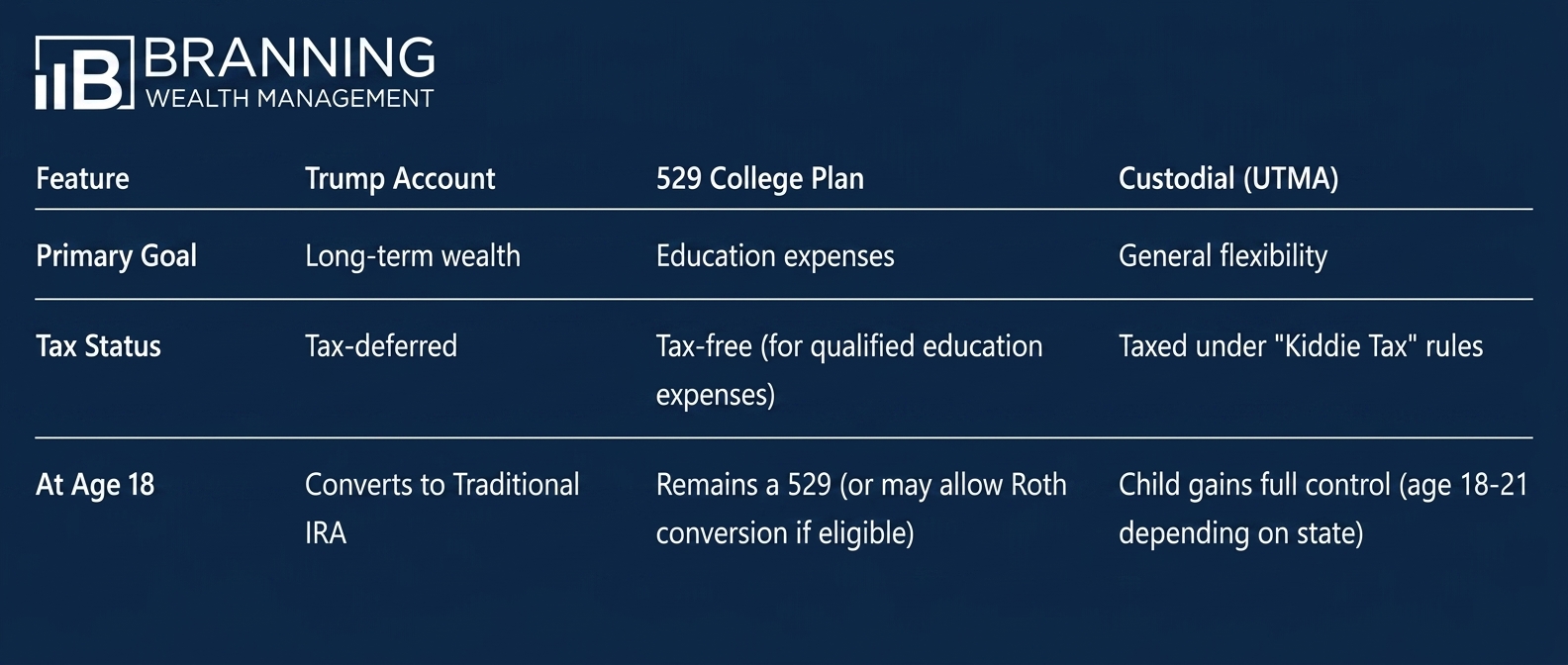

Is the Trump Account the best place for your next dollar? Depends on your goal(s). Here is how it stacks up against other investing tools.

Your Action Items

- Check Eligibility: Confirm if your child qualifies for the free $1,000 from the Fed.

- Verify the SSN: If you have a newborn, make sure that Social Security paperwork is finished.

- Talk to Your CPA and/or Financial Advisor : Discuss the new IRS election form and how contributions may affect your taxes.

- Check with HR: See if your employer has plans to offer matching contributions to Trump Accounts.

Final Thoughts

Trump Accounts are an interesting opportunity for the new generation. The true value of the Trump Account isn’t necessarily the dollars inside it today, but the financial habits it may help create over time . By seeding each account with $1,000, the government is trying to nudge families to begin the habit of investing early and teach children the power of long-term compounding. The hope is that these habits will continue the rest of their lives!

When used internationally, a Trump Account can become a cornerstone of your child’s financial foundation. The best use of a Trump Account depends on your broader financial picture, including education planning, retirement goals, taxes, and cash flow priorities.

If you'd like help determining whether a Trump Account fits into your family's overall financial plan, we'd be happy to help.

________________________________________________________________________________________________________________________

Johnson Rhett, CFP®, ChFC® is a fee-only, fiduciary financial advisor with Asset Dedication LLC, DBA Branning Wealth Management.

Want to talk? Schedule a complementary call HERE!

Disclaimer: This blog is distributed for general informational purposes only and is not intended to constitute legal, tax, accounting, or investment advice. Information in this blog is obtained from sources that we believe reliable, but BWM does not warrant or guarantee the timeliness, accuracy, or completeness of this information. All investments involve risk of loss, and nothing within this blog should be construed as a guarantee of any specific outcome or profit.